RRSP vs TFSA: Why "Tax-Free Withdrawals" Don't Tell the Whole Story - Beat the 2025 RRSP Contribution Deadline!

With the 2025 RRSP contribution deadline fast approaching on March 2, 2026, this is the question every Canadian investor is wrestling with: should I put my money into my RRSP or my TFSA? The answer might surprise you

The Misconception That's Costing Canadians Thousands

Ask a roomful of Canadians which account is "better," and most will say the TFSA. The reasoning is intuitive: withdrawals are completely tax-free. Compared to the RRSP, where every dollar you pull out in retirement gets taxed as income, the TFSA sounds like the obvious winner.

But this thinking has a major flaw: it ignores what happens on the way in.

When you contribute to an RRSP, you get a tax deduction. If you're earning $90,000 in Ontario, your combined marginal tax rate is roughly 29.65%. A $7,000 RRSP contribution generates about $2,075 back in your pocket at tax time. If you reinvest that refund — either back into the RRSP or into your TFSA — you're working with significantly more capital than the TFSA contributor who put in the same $7,000 after-tax dollars.

The math only tips in the TFSA's favour when your retirement tax rate exceeds your working tax rate. For many Canadians with pensions, high CPP/OAS income, or significant retirement savings, this isn't the case. For others — particularly those who expect to retire at a lower income — the RRSP wins by a surprisingly wide margin.

The truth is: It's much more nuanced than that. There is no universally correct answer. The right choice depends entirely on your personal situation: your income today, your expected income in retirement, your province, whether you have a spouse, children, and much more.

That's exactly why we built the RRSP vs TFSA Calculator.

When RRSP and TFSA Are Exactly Equal

Before we get into the calculator, let's clear up the math. When your tax rate is the same at contribution and withdrawal, the RRSP and TFSA produce the exact same after-tax result. This surprises a lot of people, so let's walk through a quick example.

Say you earn $1,000 and your marginal tax rate is 30% — both now and in retirement.

TFSA route: You pay $300 in tax, invest $700, it grows at 7% annually for 25 years, and you end up with $3,798. You withdraw it tax-free. Final after-tax amount: $3,798.

RRSP route: You contribute the full $1,000 (getting a $300 tax refund, which you reinvest into the RRSP). Your $1,000 grows at 7% for 25 years to $5,427. You withdraw it in retirement and pay 30% tax ($1,628). Final after-tax amount: $3,798.

Identical. The RRSP's tax deduction going in perfectly offsets the tax paid coming out — as long as the rate is the same both times.

But Things Are Rarely Equal

This is where it gets interesting, and where the calculator really shines. In the real world, your tax rate in retirement is almost always lower than your working tax rate — even if you withdraw enough to land in the same tax bracket. Why? Because of several credits and benefits that apply specifically in retirement:

- The Age Credit — a non-refundable federal tax credit available once you turn 65, worth over $1,000 in tax savings annually

- The Pension Income Credit — a credit on the first $2,000 of eligible pension income (including RRIF withdrawals after age 65), worth up to $300 federally plus additional provincial savings

- Pension Income Splitting — if you have a spouse, you can split up to 50% of your eligible pension income with them, potentially keeping both of you in lower tax brackets

These credits mean that even when your bracket looks the same on paper, your effective tax rate in retirement is often meaningfully lower.

And if you have kids, there's another advantage most people overlook entirely. RRSP contributions lower your Adjusted Family Net Income (AFNI), which directly increases your Canada Child Benefit payments. The TFSA contribution doesn't do this. So the RRSP isn't just winning on the investment side — it's putting more government money in your pocket every month while your children are young.

Before the Numbers: The Non-Financial Case for Each Account

Before we dive into the calculator, it's worth talking about something the spreadsheets don't fully capture — the behavioural and lifestyle advantages of each account type.

The TFSA Advantage: Flexibility

The TFSA is genuinely one of the most flexible investment accounts ever created. You can withdraw from it for any reason — a home renovation, a vacation, an emergency — and you don't lose the contribution room permanently. It comes back on January 1st of the following year.

This flexibility is valuable in ways that are hard to quantify. Life is unpredictable, and having accessible savings that don't come with a tax bill or lost room can provide real peace of mind. If you're early in your career and not yet sure what your income trajectory looks like, the TFSA lets you build wealth without locking yourself into assumptions about the future. If you're in retirement, TFSA withdrawals can provide great flexibility as part of your plan. For example, if you need more income, but don't want to trigger OAS clawback, TFSA withdrawals work great as they don't count towards your income.

The flip side, of course, is that this same flexibility can work against you. When money is easy to pull out without consequence, it's easier to rationalize dipping into it. For people who struggle with the temptation to spend savings, the TFSA's flexibility can quietly undermine long-term wealth building.

The RRSP Advantage: Built-In Friction (Yes, That's a Feature)

The RRSP's restrictions are often seen as downsides, but for long-term investors, they can actually be a feature. Withdrawing from an RRSP for anything other than the Home Buyers' Plan (HBP) or Lifelong Learning Plan (LLP) means losing that contribution room permanently — and paying income tax on the withdrawal on top of it. That's a significant psychological barrier that tends to keep money invested.

Speaking of the HBP and LLP: these are genuinely powerful programs that deserve more attention.

- The Home Buyers' Plan lets first-time homebuyers withdraw up to $60,000 from their RRSP tax-free (as of 2024) to put toward a home purchase. You repay it over 15 years. It's an excellent way to use RRSP savings for a major life goal without a permanent tax hit.

- The Lifelong Learning Plan allows you to withdraw up to $10,000 per year (to a $20,000 lifetime limit) from your RRSP to fund full-time education for yourself or your spouse. Again, repayable over time, and a smart option if you plan to return to school.

If either of these situations applies to you, the RRSP becomes more compelling as a savings vehicle.

What's Better For You: Using the RRSP vs TFSA Calculator

Our calculator goes well beyond a simple comparison. It models your entire financial journey from today to the end of retirement, accounting for taxes in both phases, government benefits, and family situation. Here's how to use it.

Step 1: Enter Your Basic Details

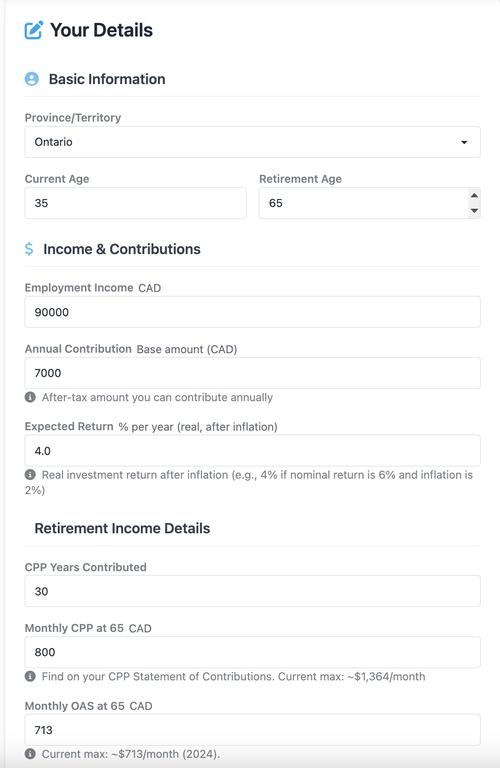

Start with the basics. Select your province or territory — provincial tax rates vary significantly across Canada, and this has a real impact on your results. Enter your current and estimated retirement age, your employment income, and the annual after-tax amount you're planning to invest.

The Expected Return field asks for a real return — that is, after inflation. If you expect a 6% nominal return and inflation runs at 2%, enter 4%. This is the right way to model long-term projections because it keeps all the dollar figures in today's purchasing power, making them easier to interpret.

For the retirement income section, enter your CPP and OAS estimates. You can find your CPP projection on your My Service Canada account. The calculator notes the current maximum OAS of ~$713/month as a reference point.

Step 2: Add Your Family & Tax Situation

This is where the calculator gets genuinely powerful — and where most simple RRSP vs TFSA comparisons completely fall short.

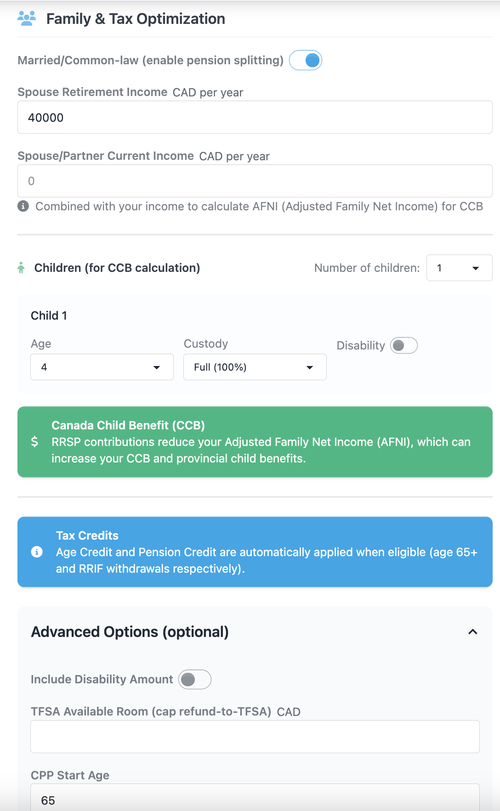

If you're married or common-law, toggle on the spouse option. The calculator will model pension income splitting in retirement, which can dramatically reduce your combined tax bill by shifting income from the higher-earning spouse to the lower earner. This is a major advantage for couples with unequal retirement incomes.

You can also enter your spouse's current income, which factors into the Adjusted Family Net Income (AFNI) calculation for the Canada Child Benefit — and this is where one of the most overlooked RRSP benefits comes in.

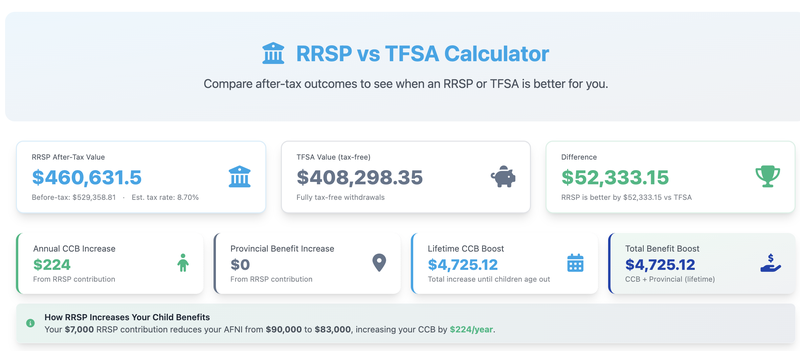

RRSP contributions reduce your AFNI. A lower AFNI means a higher Canada Child Benefit. In the example shown in the calculator, a $7,000 RRSP contribution on a $90,000 income with one 4-year-old child increases the annual CCB by $224. Over the years until that child turns 18, that adds up to $4,725 in additional child benefits — completely aside from any investment growth. That's real money that most people never account for when comparing RRSP vs TFSA.

Step 3: Review Your Results

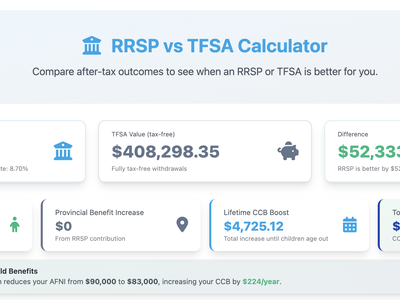

The results section (at the top) gives you the bottom line clearly and without jargon. In this example scenario — an Ontario resident earning $90,000, contributing $7,000/year, retiring at 65 — the RRSP comes out ahead by over $52,000 in after-tax value compared to the TFSA.

Notice that the calculator shows the RRSP's after-tax value (not the before-tax balance), so you're comparing apples to apples. It also shows the estimated effective tax rate on RRSP withdrawals in retirement — in this case, just 8.7%, which is significantly lower than the 29% marginal rate at the time of contribution. That gap is the source of the RRSP's advantage.

The CCB boost is shown separately: $224 per year, $4,725 lifetime. This isn't added to the investment balance — it's modelled as additional money in your pocket from the government, because the assumption is you'd spend it rather than invest it. If you did invest it, the RRSP advantage would be even larger.

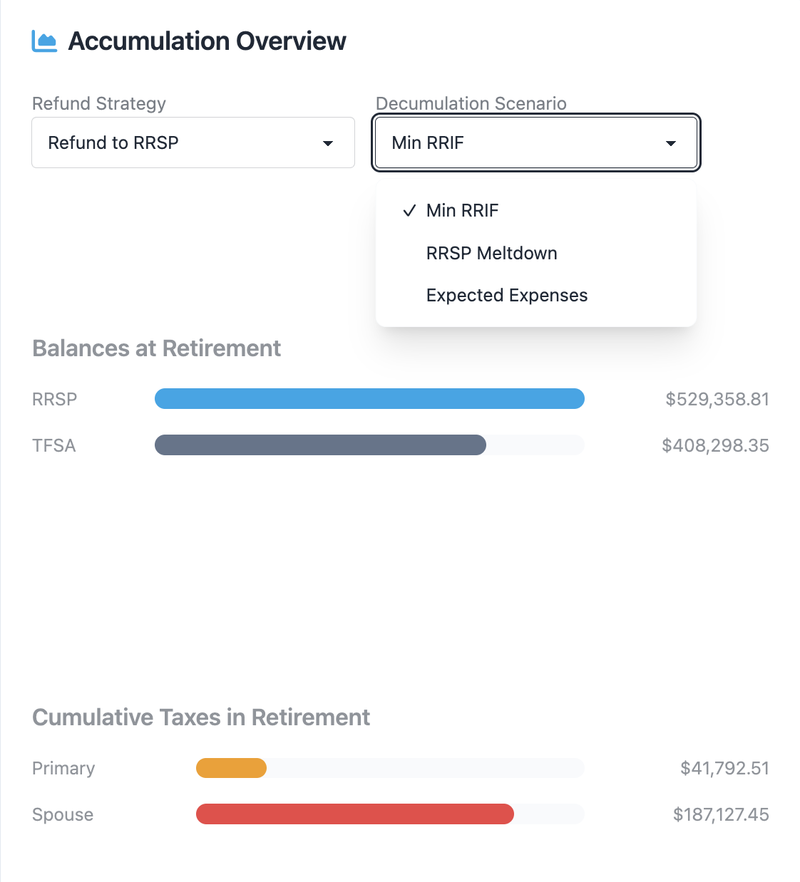

Step 4: Explore Decumulation Strategies

One of the most sophisticated features of the calculator is the ability to model different decumulation scenarios — how you draw down your savings in retirement.

- Min RRIF: The government requires RRSP holders to convert to a RRIF by age 71 and withdraw a minimum percentage each year. This option models exactly that minimum withdrawal schedule.

- RRSP Meltdown: This strategy involves withdrawing from your RRSP more aggressively before retirement or in early retirement, at a time when your income is lower. The goal is to reduce the RRSP balance before mandatory minimums kick in at higher rates, potentially avoiding OAS clawback later in life. This also helps avoid a large tax to your estate on death.

- Expected Expenses: Model your withdrawals based on what you actually expect to spend in retirement.

You can also choose a Refund Strategy: reinvest your RRSP tax refund back into the RRSP (maximizing the compounding effect), or redirect it to your TFSA (which keeps the TFSA growing and provides more tax-free income in retirement).

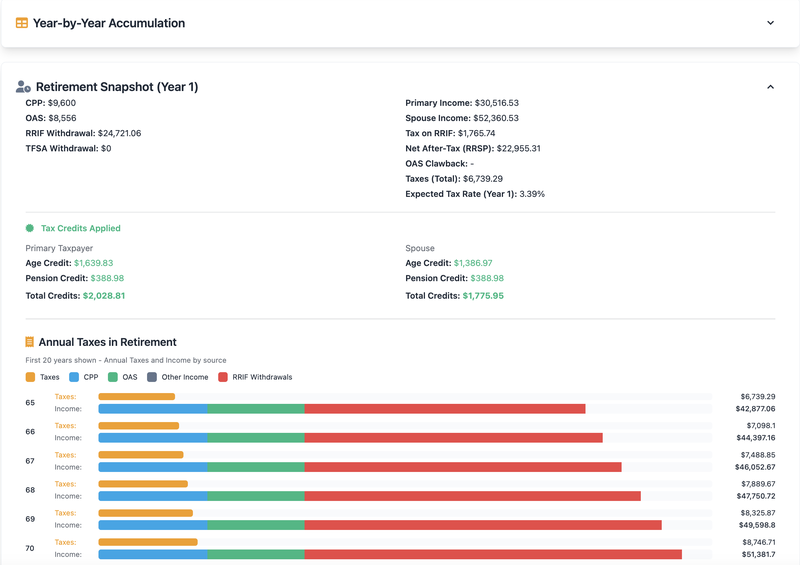

Step 5: See the Year-by-Year Picture

The detailed year-by-year breakdown is where you can really dig in. For each year of retirement, the calculator shows your income sources (CPP, OAS, RRIF withdrawals, TFSA withdrawals), the taxes you'll pay, and the tax credits applied — including the age credit and pension income credit that kick in at 65.

The bar chart showing Annual Taxes in Retirement is particularly useful for spotting years where you might face OAS clawback, or where strategic withdrawals from the TFSA versus the RRIF could reduce your tax burden.

So, Which Should You Choose?

Here are some general principles, though the calculator will give you numbers specific to your situation:

The RRSP tends to (but not always) win when:

- Your income today is significantly higher than your expected retirement income

- You plan to reinvest your tax refund

- You have children and can benefit from the CCB boost

- You're married with unequal incomes (pension splitting helps)

- You're a first-time homebuyer or planning to return to school

The TFSA tends to (but not always) win when:

- Your income today is low or you expect similar/higher income in retirement

- You don't have a spouse, or your spouse will have similar income in retirement (no income splitting)

- You have a generous pension or other retirement income sources

- You value flexibility and may need to access funds before retirement

- You've already maximized your RRSP contribution room

The honest answer for most people: For many people, a combination of both TFSA and RRSP is a good option. This provides the flexibility with the TFSA along with the often higher net return of the RRSP.

The RRSP Deadline Is Coming

The deadline to contribute to your RRSP and have it count against your 2025 tax year is March 2, 2026. If you're still on the fence, there's no better time than now to run the numbers.

Try the RRSP vs TFSA Calculator →

You can also read the full methodology and constants used in the calculator if you want to understand exactly how the numbers are calculated — including the provincial tax brackets, RRIF minimum withdrawal rates, and CCB phase-out formulas.

As always, this isn't personalized financial advice. Every situation is different, and for complex scenarios it's worth consulting a fee-only financial planner. But armed with the right tools and a solid understanding of how these accounts actually work, you're already ahead of most investors.

Stay Updated

Get the latest investment insights delivered to your inbox. We will not spam you with emails. Emails will be limited to around one per month, and may contain relevant market updates, new features, or new blog posts.

Image Gallery

More Articles

Market Analysis

Stay informed with our latest market insights and analysis.